Guide to open a physical Gold Savings Plan

How traditional Pension and Savings Plans work

When it comes to retirement savings or pension plans, what do you imagine?

- Make contributions year after year in the hope of obtaining a significant return in the future?

- Without being able to have your money until a expiration is met?

- Once we can withdraw our money pay a large amount of taxes?

You are not the only one. These options make up the majority of traditional savings plans, such as retirement plans. And for many, they are the only place where they keep their long-term savings.

Unfortunately, these traditional options offer neither the security nor the flexibility that most people require.

This all adds up to the fact that most traditional savings plans offer zero flexibility and (worse) can be completely decimated by economic turmoil, slumps, and stock market crashes..

And for those who have spent years and decades of their lives saving money for a more comfortable future ...

There's nothing more frustrating than 20-30 years of savings going down the drain in a matter of weeks.

If you want a plan for the future that protects you and your family, this is the best gold savings plan that I know.

Traditional Retirement Plan vs. Gold Savings Plan: Analyzing Your Options

Retirement Plans / Savings Plans:

- Little or no direct control over investments

- Impossibility of early withdrawal except in cases of force majeure except penalties

- Lack of liquidity in times of greatest need

- Strict monthly or annual contribution limits with legal penalties

- Subject to financial market volatility (a decades-old investment can disappear in a single week)

Gold Savings Plan:

- 100% assigned gold (buy, sell, store; do what you want with it)

- No withdrawal, transfer or hidden fees

- Contribute with the amount you want -a lot or a little-, without limits

- Maximum liquidity (withdraw whenever you want without penalties)

- Ability to invest in the historically most stable commodity during pandemics and economic crises

Profitability of more than 500% in the last 20 years

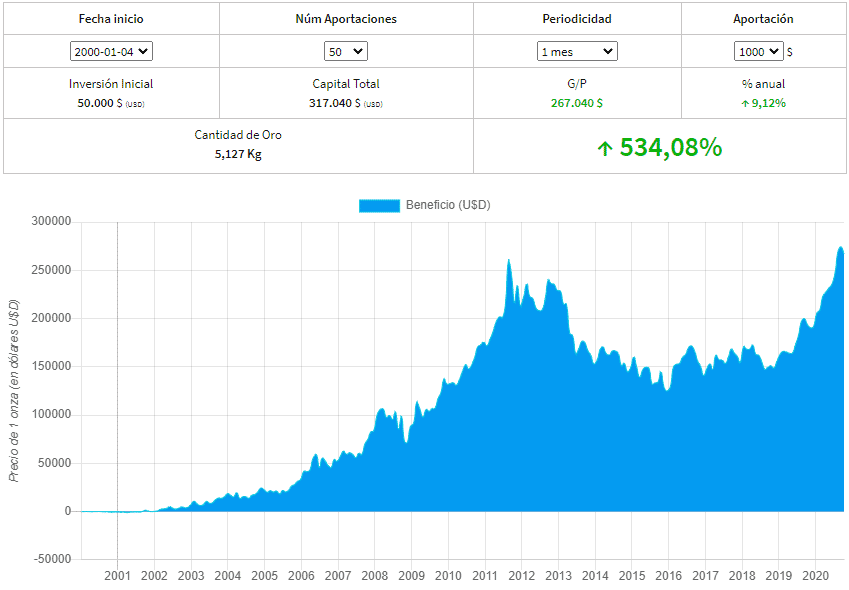

In the last 20 years, from 2000 to 2020, we would have obtained a 534% profitability if we had followed a gold savings plan.

Suppose we had started a gold savings plan in January 2000 with the following characteristics:

- Monthly amount: $ 1,000 dollars -to not carry out currency conversion EUR-USD-

- Number of contributions: 50

- Periodicity: once a month

- Total Investment: 50 x $ 1000=$ 50,000

In view of the graph, we see that the net profit would have been $ 267,040, or what is the same, a annual return of 9.12% and a total capital of $ 317,040.

This is the advantage of carrying out a capital accumulation plan, or what is the same, regular contributions over a certain period, since we average in price and from this In this way we also avoid the risks of volatility of the underlying asset.

Obviously, we cannot guarantee that gold will behave the same way in the next 20 years, but the following criteria can help:

- It is a rare commodity in nature

- More and more electronic devices use small parts of gold for their conductive properties

- There is a large accumulation of gold bars in countries such as the United States, China, India, Russia and Germany.

Gold has always maintained its value

Creating a gold savings plan is the best way to prepare your savings for the future, protect against inflation and ensure complete control over your assets .

That is why investing in gold has always been the best way to protect your wealth.

That's because investment gold is:

- Resistant (and almost immune) to inflation.

- A commodity that maintains its value (and even increases) in times of economic turmoil.

- Has an inherent physical value (not like ETFs).

- Highly liquid when owned exclusively by you (also known as "assigned gold") and with the right storage partner.

- Gold, then, is obviously the best savings option compared to traditional savings plans, such as pension plans or PIAS.

But the question is, who should you trust when creating your gold savings plan?

We will answer this question later.

Before we will talk about the risks that physical gold can have

Risks of Investing in Physical Gold

Apart from the intrinsic risks of investing in physical gold, due to counterfeits and the problem of storage, since it is a small-sized but high-value good, the main problems are:

- Risks of paper gold (ETF, futures)

Does not own physical gold. It is one of the most common options today, where the amount of contracts being traded are not backed by physical gold.

To give you an idea, about 8,000 - 10,000 million dollars of physical gold are traded / year, while the volume of paper gold is about 20,000 - 30,000 million dollars / day. As you can see, there is a huge imbalance and this is the reason why ETFs are not backed by gold reserves.

- Unallocated Gold Risks

The most common thing is that the client trusts the bank that guards the gold that he has bought, among other things because the client himself would not know what to do with it in his house. The customer is not the owner of the gold, but a creditor of the bank. For this reason, the bank can dispose of this gold for its own reserves and trade with it in case of liquidity problems.

- Risks of assigned gold

Even having your assigned gold is not without risk. According to the newspaper Oroinformación, several Swiss banks have had no qualms about using the gold bars assigned to clients to negotiate with them.

The situation has been resolved because there was enough metal on the market, but what would have happened if there was not enough?

So even though the gold is assigned, leaving it in the hands of the bank for safekeeping is a risk.

Experts recommend that even if it is assigned gold, it is not convenient to leave it in the safe deposit boxes of the banks since by the "Bail In" law - banks can recapitalize from bank assets - banks can make use of the metal in case of crisis or solvency problems.

- Risks of physical gold

The main problem is counterfeits and, as we have seen, they tend to be more and more perfect.

Therefore, to avoid risk as much as possible, the main thing is to have an operator that guarantees total security when investing in gold and offers the guarantees and quality certificates that ensure the purchase of gold or precious metals as well as their storage.

How does Auvesta's gold savings plan work?

It is an alternative to traditional pension plansonales, without the inconvenience or penalties to get our money back.

The company that I know and where I have my savings plan is Auvesta, a German multinational present in more than 100 countries.

Auvesta is the leader in precious metal savings products (gold, silver, platinum and palladium) in Europe according to Focus Money magazine, in addition to being awarded by the German Ministry of Finance as:

- best precious metals trader,

- best price,

- best service and

- greater transparency.

Let's see the operation of the gold savings plan:

- You can make contributions as, when and how much you want,

- The period and the amount is up to you, you do it at your own pace

- You can get your money back in precious metal whenever you want

- They only ask you for a deposit of € 2,250 (in the case of savings plans) to pay the insurance and deposit expenses, which they return to you with 5% bonuses of the contributions you make.

In case of withdrawing your money, your deposit will continue to be recovered through contributions.

The first payment is the deposit, € 2,250 + the amount you want to start saving periodically

If you make a contribution of € 1,000 they add an extra bonus of 5%, I explain it better in the following table:

| Savings Plan Simulation - Premium Account | |||||

|---|---|---|---|---|---|

| # month | contribution | bonus 5% | gold quantity | total gold | remaining deposit |

| 0 | 3250€ | 50€ | 1050€ | 1050€ | 2200€ |

| 1 | 1000€ | 50€ | 1050€ | 2100€ | 2150€ |

| 2 | 1000€ | 50€ | 1050€ | 3150€ | 2100€ |

| 3 | 1000€ | 50€ | 1050€ | 4200€ | 2050€ |

| 4 | 1000€ | 50€ | 1050€ | 5250€ | 2000€ |

| ... | |||||

How to open the gold savings plan step by step?

To open a plan in Auvesta, it is very simple. Here I explain it to you step by step:

1. Click on the following link:

2. Once inside the Auvesta page you have to click on the button "Register"

3. Once clicked, a form will appear where you have to enter your personal data and check the "I'm not a robot" box.

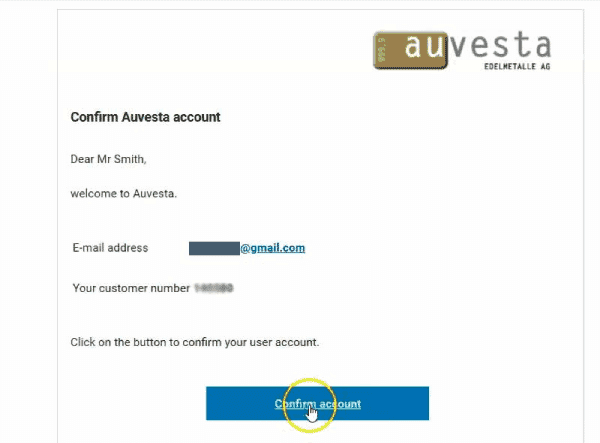

4. When you fill in your data, another screen will appear where you will see that the user has been created

5. Then you should check your email and verify that you have received an email with the subject "Confirm Auvesta account"

And confirm the account by clicking on the button "Confirm Account"

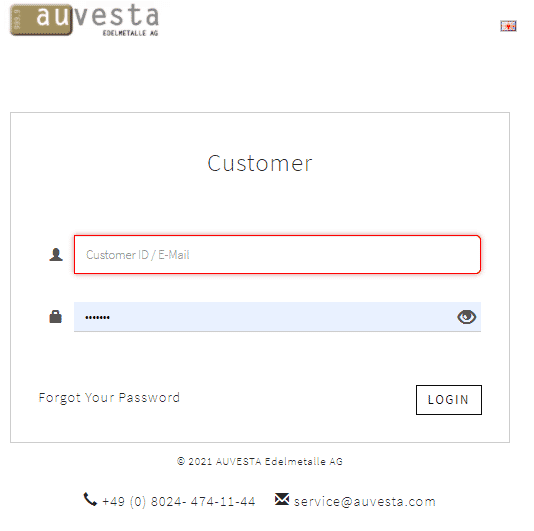

6. When you confirm your email, it will take you to the account login screen where you will have to enter the login data in your account: email and password.

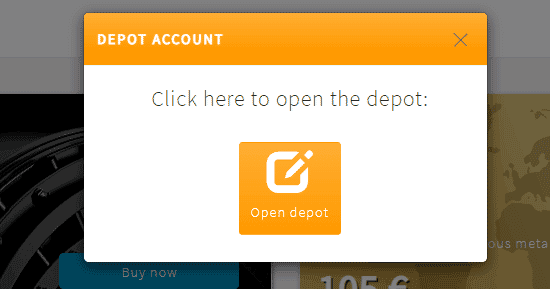

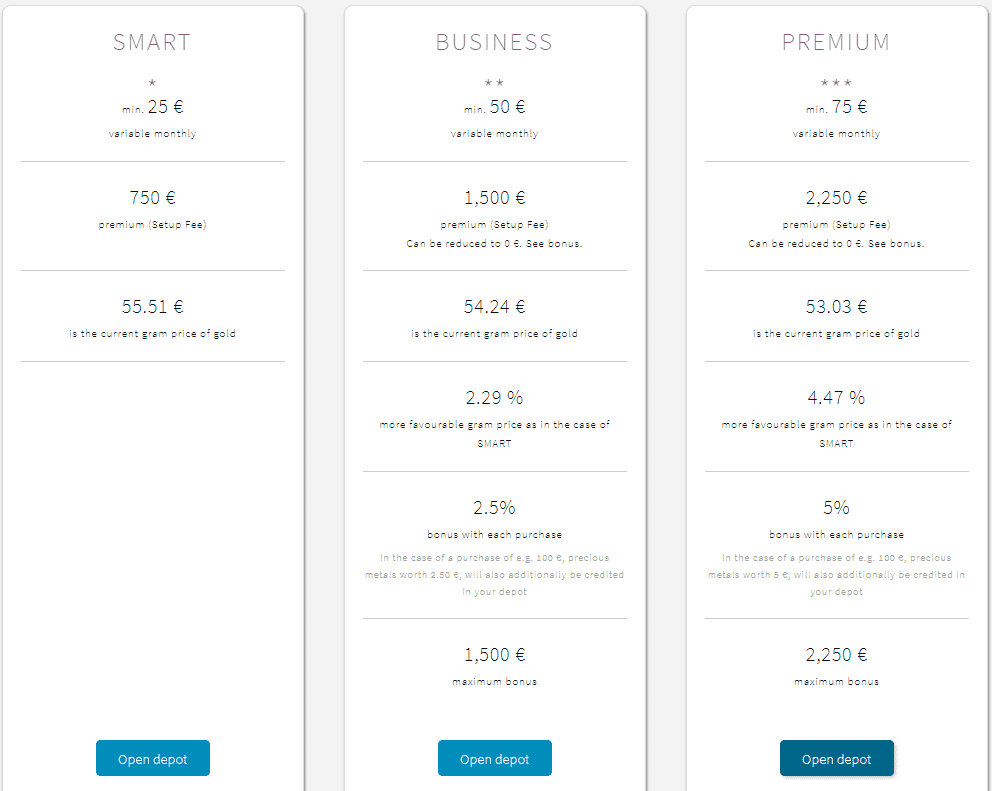

7. Once inside your account you must click on the "open deposit" button:

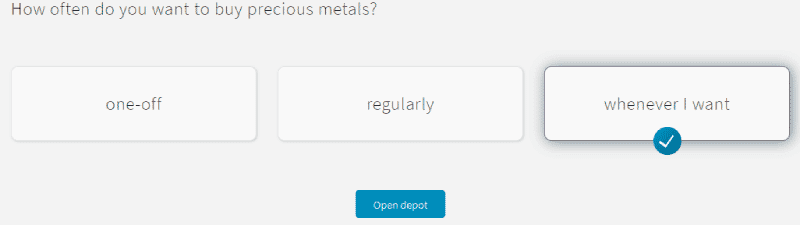

8. Now we are going to choose what type of account we want:

- savings plan: then we click on "whenever I want" or "regularly"

- investment account: for amounts from € 50,000 we mark "once". Even if you put only once, we can make contributions later.

We mark the one we want and click on the button "** open deposit **"

9. Once you have decided the frequency of the contributions, you can choose the type of account you want.

If the plan is a savings plan, we will choose the premium account, since it is the only one where we can recover the entire premium.

The Smart and Business accounts, in addition to having the most expensive price, do not allow us to recover the initial premium in full.

-

If we start with the full premium, that is, with more than € 2,250, then we can benefit from a 5% bonus for each contribution above € 2,250.

-

If we start with less amount of the premium, then 70-30% will be made.

That is, 70% of the amount we enter will go to complete the premium and 30% to the purchase of metal, but we will not have any bonus until we complete the premium.

We click on "Open deposit"

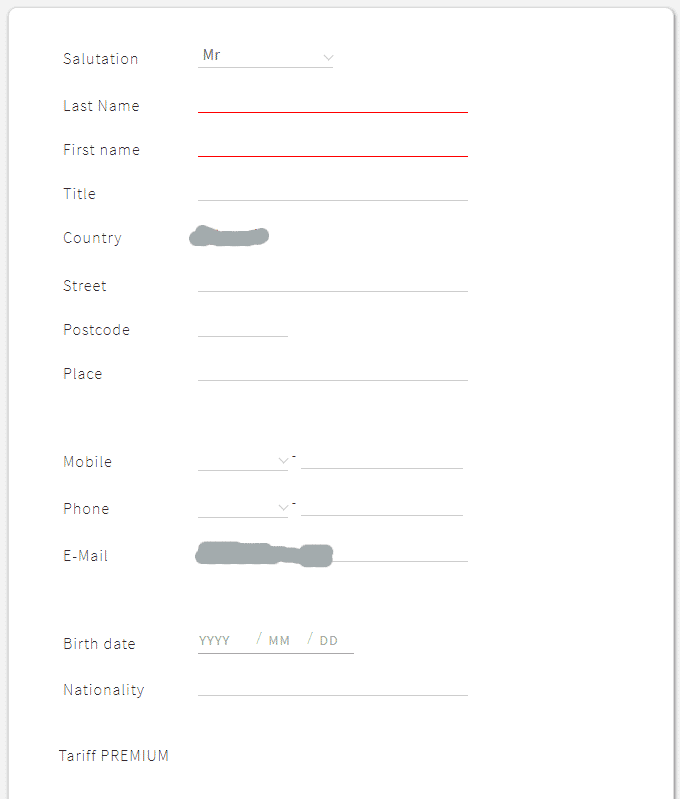

10. Now you should see the data with which to start the account you have chosen and you just have to click on "Open Deposit"

In this part we see the data with which we registered and we will also have to put some new ones

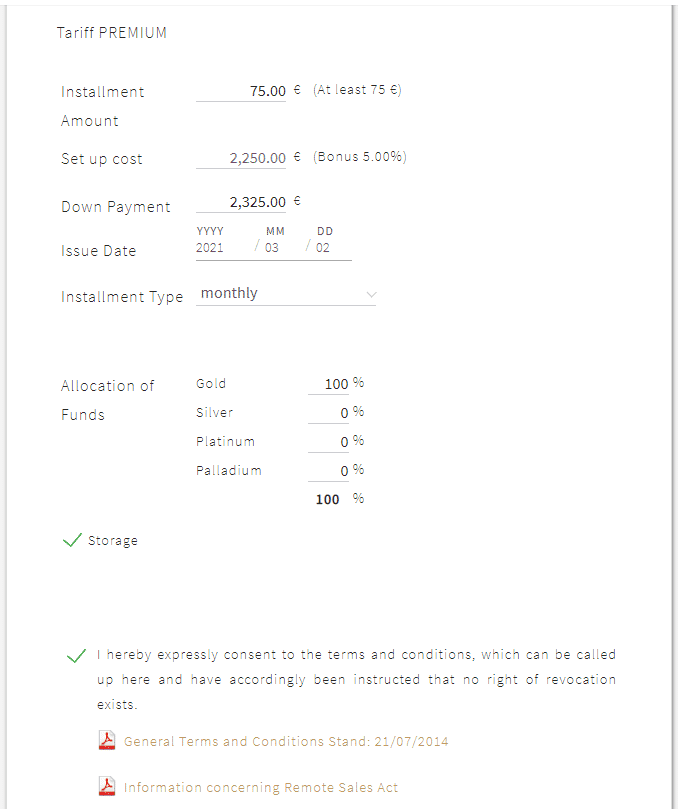

In this part of the form we enter the account start data.

- Amount fee: At least € 75.00, but you can put whatever you want

- Premium: € 2,250

- Premium ticket:

- Full contribution of the premium, we will start with € 2,250 + € 75 of the amount of the fee=** € 2,325 **

- If we do not make the full contribution we will enter the amount with which we will start, from € 100 whichever we want: € 500, € 1000, € 1500.

We can choose the quantity destined to gold, silver, platinum or palladium. By default it is 100% to gold, although we can change it now or later.

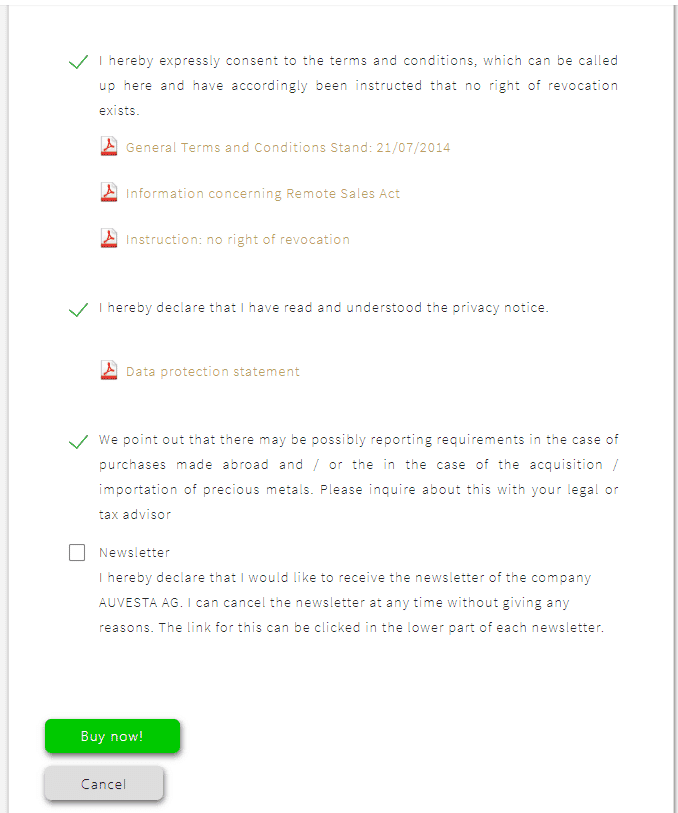

We mark all the boxes if we agree with the conditions and when we mark all the "Buy now" button below it will turn green.

We click and our deposit will be created.

We upload the documents from our account control panel

You will receive 2 emails:

- one with your account information and the password to enter

- another with bank accounts where to make the first contribution. We chose the nearest bank account.

The company has procedures to comply with the money laundering law, so the first contribution is by bank transfer, then you can make the contributions by credit card or paypal.

Here is the link for you to open your deposit in gold:

If you have any questions contact us and we will clarify them